Is SpaceX, Anthropic and OpenAI overvalued?

An Amazon reminder to contemplate

Whether or not SpaceX is overvalued right now is the wrong question to think about. Profiting from SpaceX being overvalued is unactionable. Are any of the people claiming SpaceX is overvalued right now shorting the stock? No.

What percentage of people that believe SpaceX is overvalued will buy put options or sell call options in the coming weeks? Close to zero.

A critique of my first two paragraphs might be that a) options are too risky for the average person (I agree with this) and b) SpaceX has a low float of 4 to 5% of shares, this makes shorting the stock expensive and impractical. The company has a low float because Elon Musk has most of the shares and he’s holding onto them. So what? Demand exceeds supply. This shows competency from Musk.

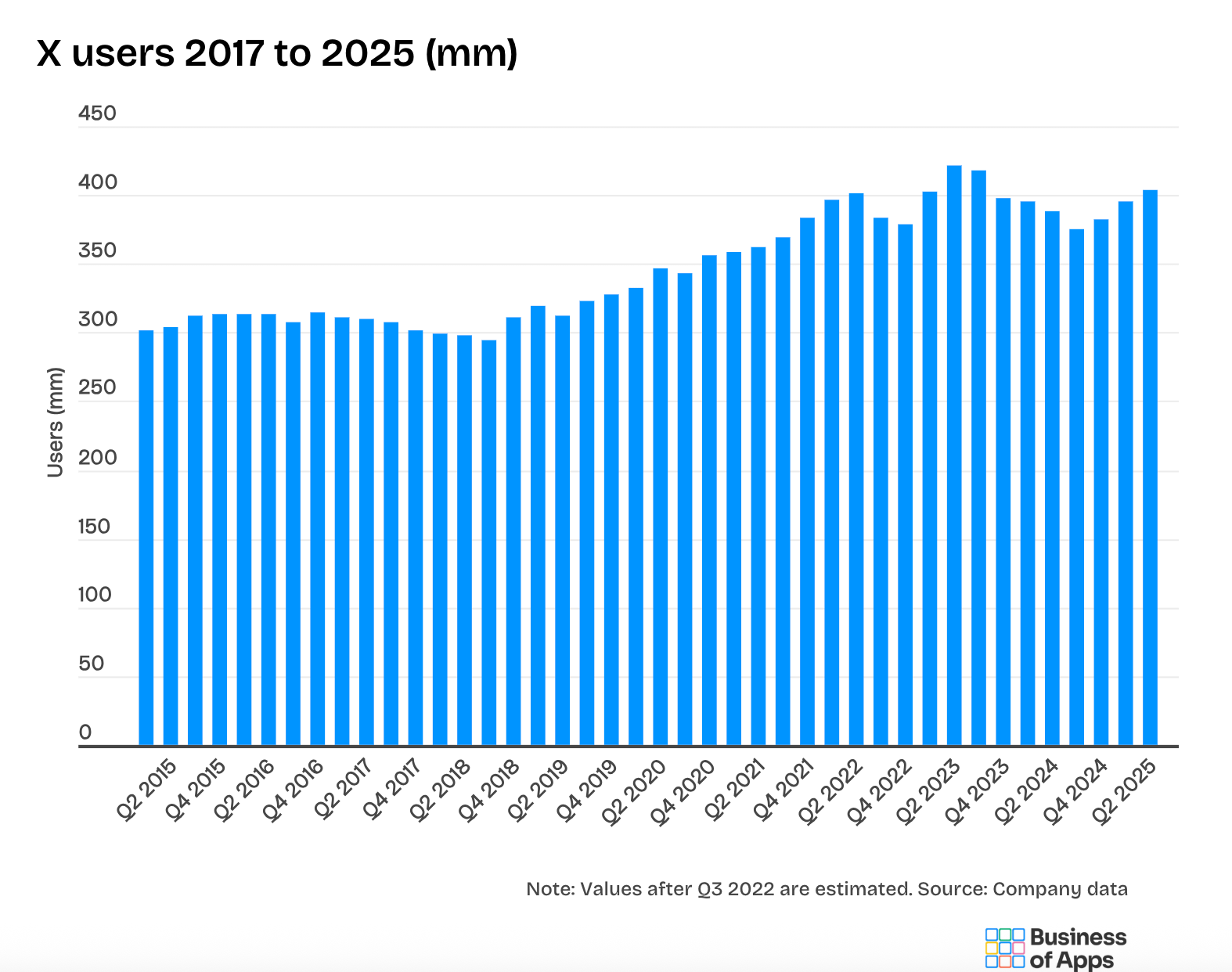

My other thought is not to underestimate SpaceX’s communications and distribution advantage. x (fka twitter) as a standalone business might be mediocre or even bad, but if you contextualize x as a direct to consumer distribution platform, then it’s actually not bad. Elon Musk in conjunction with controlling x means that SpaceX does not need to spend money on traditional marketing and has audience mindshare always.

Henry Blodget was famously barred from the securities industry on April 28, 2003 during the dot com bubble. Amazon’s market cap at the time was around $11.4 billion. A big reason was the consensus belief that Blodget was overvaluing Amazon. Amazon’s market cap today is $2.68 trillion dollars. Amazon’s market cap is 234X larger now than when Blodget was banned. His crime was overvaluing Amazon but in fact, he undervalued the e-commerce market leader.

I bring this up because we have the same situation in AI.

Last month, I attended the AAAIM Venture Summit in New York. There were a large number of AI skeptics in the audience. One statement that stuck out to me was from Amy Wu Martin of Menlo Ventures. She talked about how historically the number of startups that maintain valuations over $5 billion is small. It’s likely the middle companies that are overvalued. The market leaders and the early stage companies represent the opportunity.

The right question is, “who will be the market leader in AI?” The market leader will be undervalued twenty years from now. Recall the Amazon example.

My intuition tells me that of Anthropic, OpenAI and SpaceX, at least one will end up being massively undervalued.

If you want a safer bet in AI, I’d increase allocation into Google (aka Alphabet). Alphabet has a 4.5 trillion market cap and 28.19 P/E ratio as of now. It has comparable talent to OpenAI, Anthropic and SpaceX but with greater resources and revenue stability from other revenue streams.