AI Glasses Landgrab: Gentle Monster, Warby Parker and Oakley

Meta and Google compete for eyewear brands. Apple and Snap stay solo.

Google has acquired a 4% stake in Gentle Monster for $100 million. This follows Meta's 5% stake in EssilorLuxottica (Ray Ban, Oakley) for roughly $5 billion last year.

Why are tech conglomerates so keen on economic entanglement with eyewear companies? Eyewear is the beach head for two high priority AI strategic priorities:

Conversational AI usage

Video Data Ingestion

Apple had a stranglehold on audio with their AirPods, but glasses offer Meta a path to directly compete on audio with Apple.

Glasses are the perfect device for collecting multi-modal data through conversational AI and video / images from the real world.

Meta vs Google Alliance

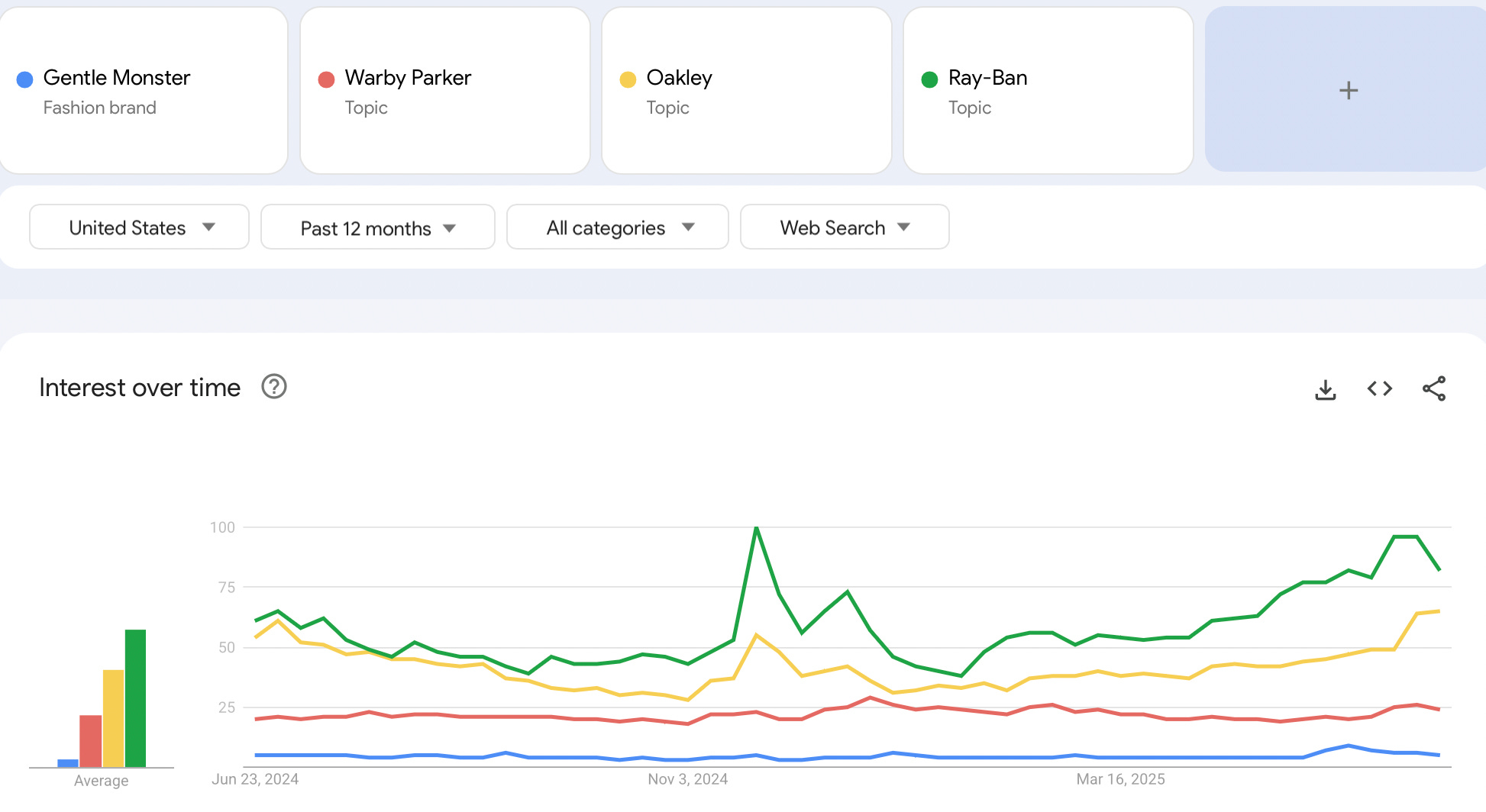

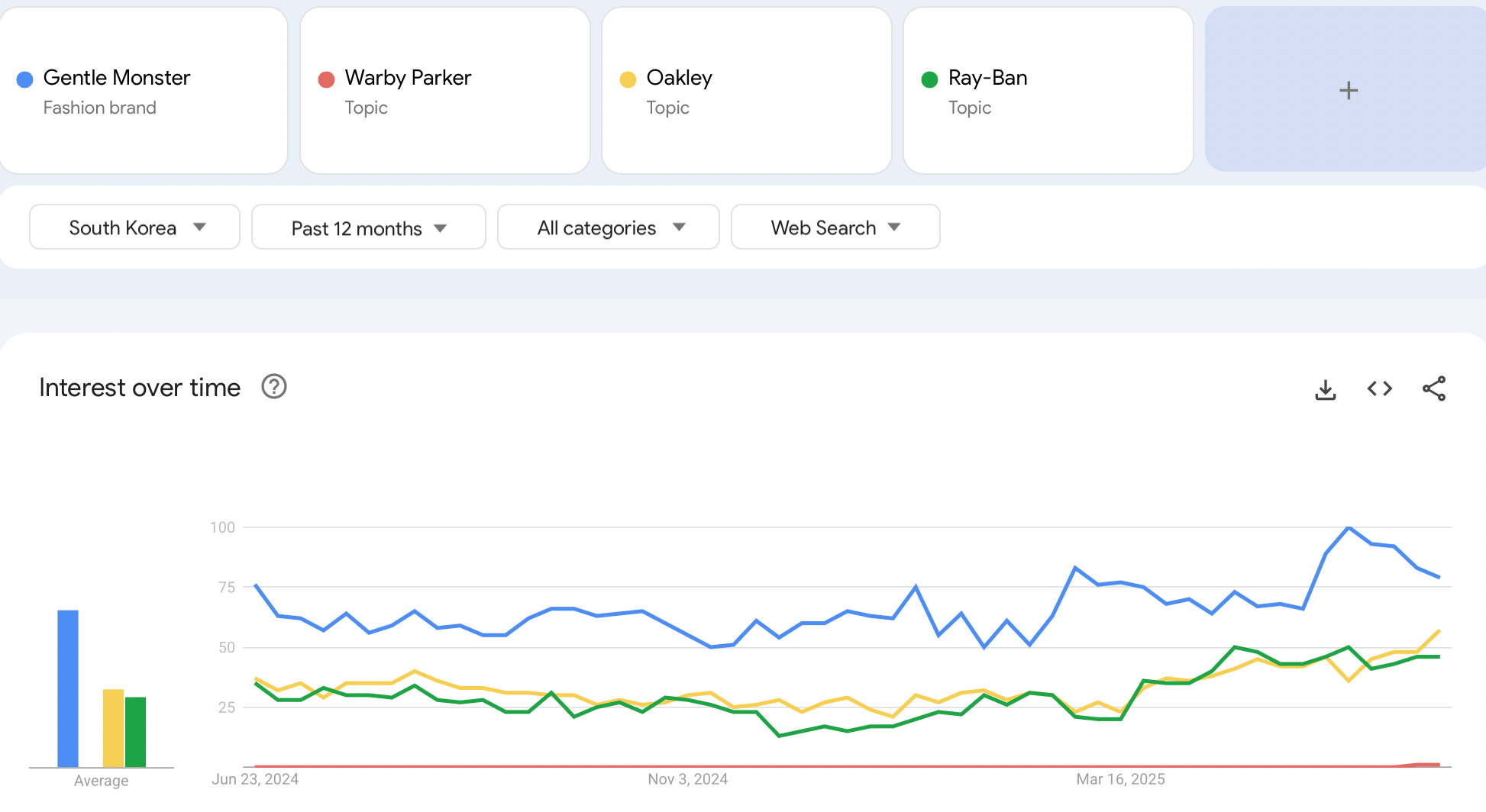

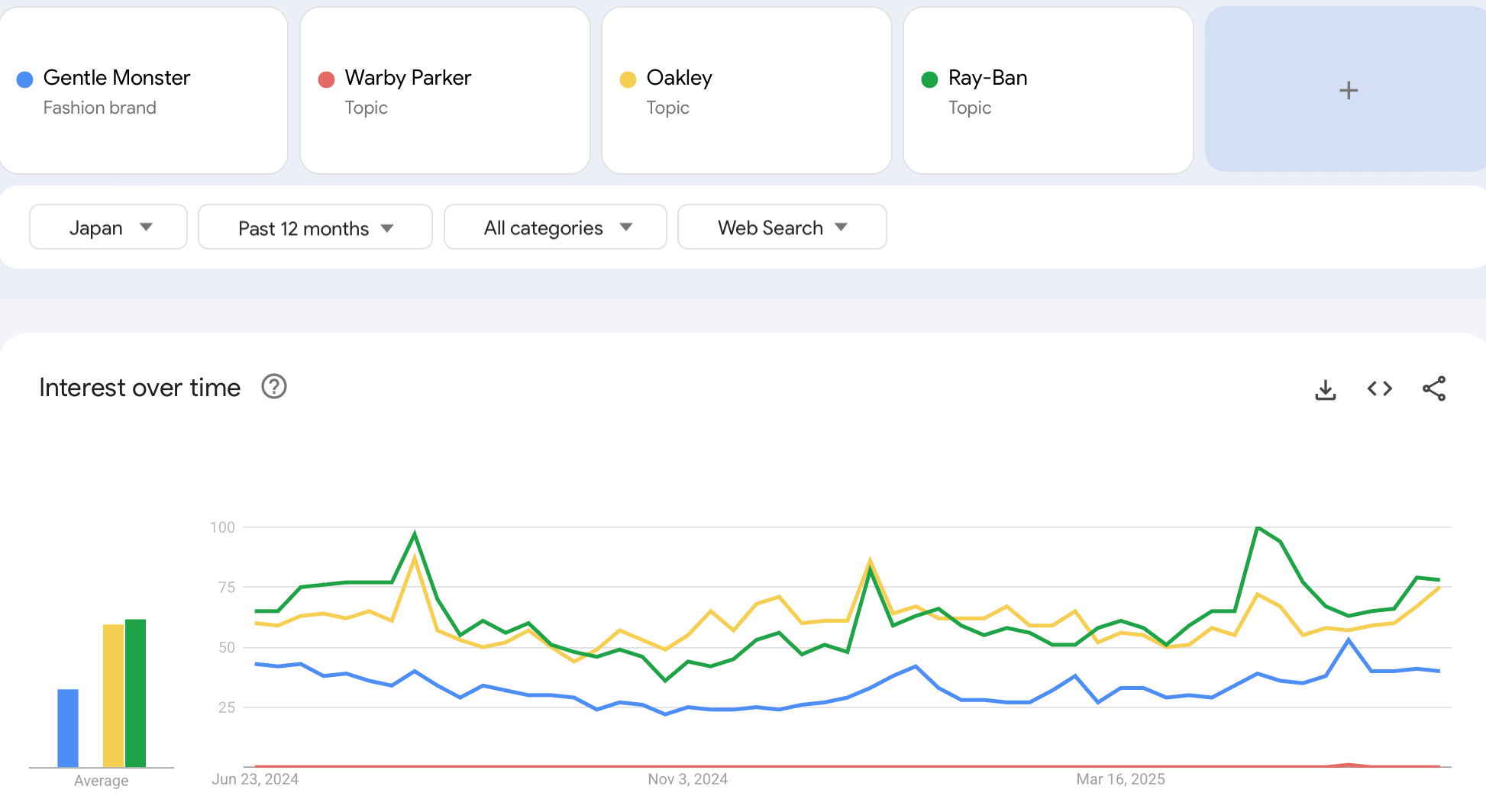

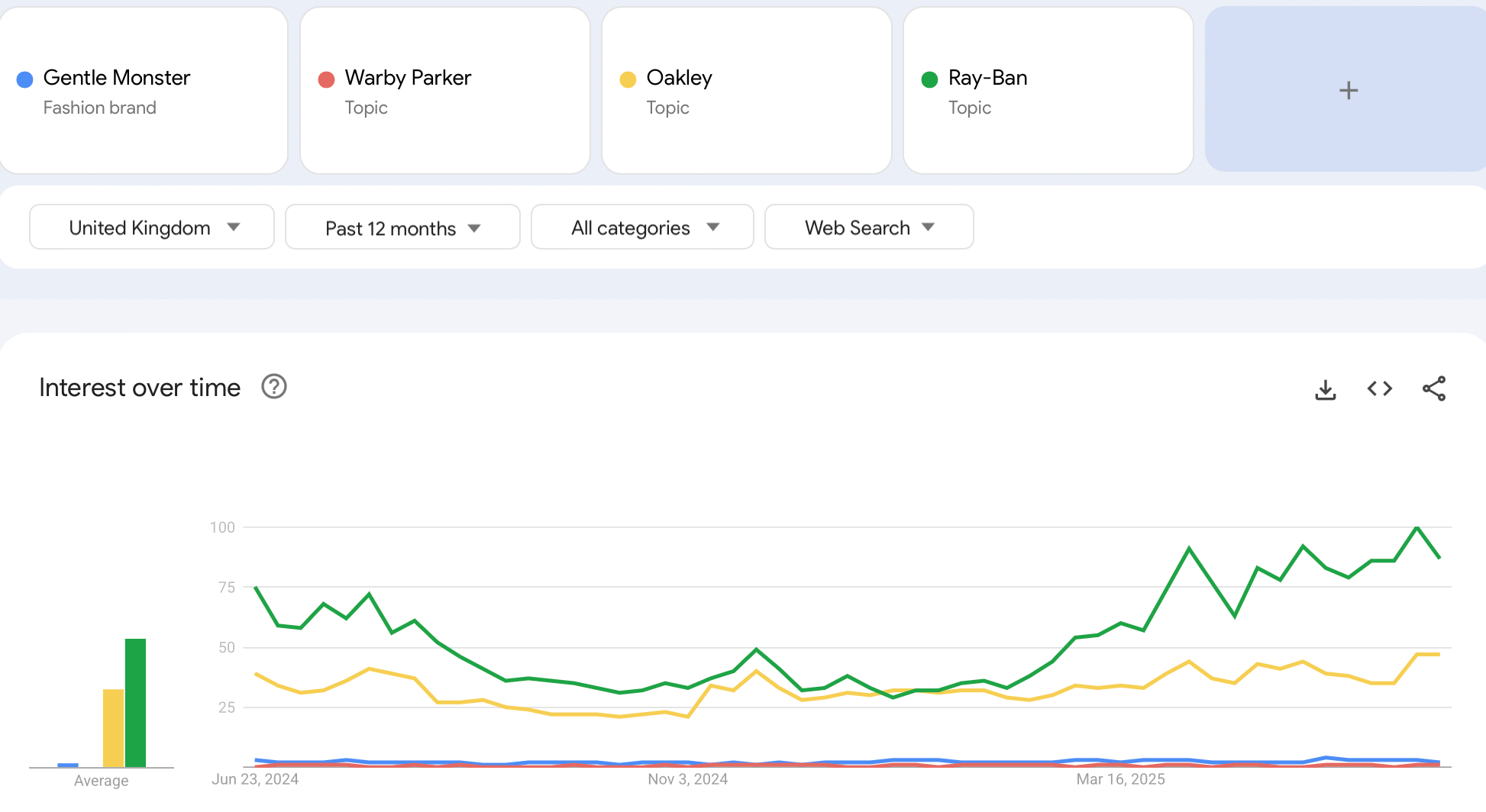

Gentle Monster is a less well known brand but it has more social cachet overall and is considered a premium brand relative to Ray-Ban and Oakley. Let’s take a look at search interest for team Google (Gentle Monster, Warby Parker) vs Meta (Oakley, Ray-Ban) in Korea, Japan and the UK.

Google is positioned to be competitive in Asia with Gentle Monster alone. Although Meta is more strongly positioned for an early advantage in greater Europe. Most European countries show similar trends to the UK in terms of search interest.

It behooves Google to put a ring on it with Warby Parker metaphorically with a stake in Warby Parker. Warby Parker is an Android XR partner but there is no economic entanglement.

China based Huawei collaborated with Gentle Monster on Smart Glasses in 2020 and 2021. They now find themselves on the outside looking in. The biggest beneficiary of Huawei getting squeezed out is likely going to be Qualcomm.

Google should act fast to avoid getting squeezed out of Warby Parker. The same way Huawei was squeezed out with Gentle Monster despite an early collaboration.

Samsung’s Mimetic Errors

Samsung’s big weakness is they only act after Apple acts. My take is that because Apple hasn’t acted yet on glasses, Samsung hasn’t either. A mimetic error.

Samsung’s HMD device (Project Moohan) looks better and is more reasonably priced than Apple’s Vision Pro. The problem is the AVP (and HMDs) didn’t take off. This is going to end up being an unused Christmas gift.

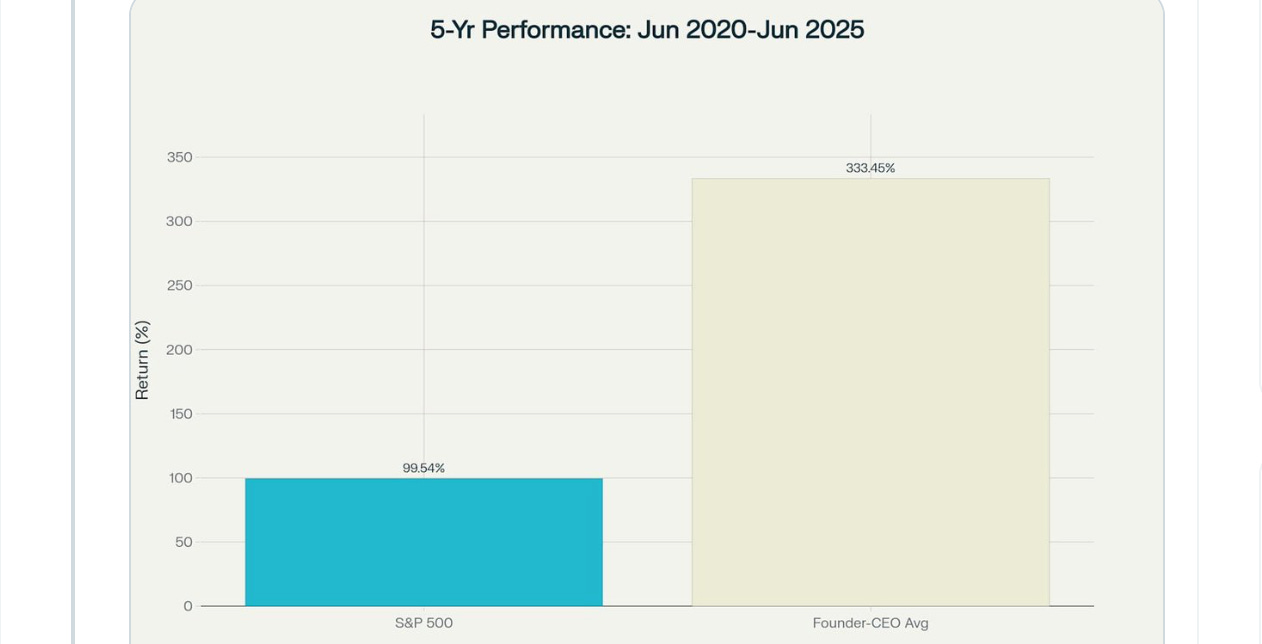

Founder Led Companies

I saw a tweet from Talia Goldberg on the difference in performance between founder led companies vs non founder led companies. The graph blow is striking.

Meta is in the lead. It’s also the only company with an active founder CEO.

Google has founders that poke around but are not active in running the company. Google is second in the AI glasses race.

Apple is lagging behind both. There are people out there that will say but Apple never comes out with product first and still wins the market. To which I say, this was true with Jobs. Under Cook, the ability to enter late and win has not continued.

Samsung is likewise a step behind because they are imitating the wrong competitor.

What about Snap?

Snap is still founder led. They all-in on AR glasses. Snap does not have eyewear brand partnerships and has a consumer focus.

The reader base of this newsletter is more likely to be interested in AR than the average person. Yet only 43% of readers indicated that they would wear the Meta Orions daily.

People have very high standards for what they are willing to wear on their face daily. I won’t count out Snap because they are still founder led.

Eyewear brands represent real estate on people’s faces. This future real estate is the key to conversational AI dominance and real world data ingestion.

Apple and Snap do not have eyewear brand partnerships yet. Do you think they are necessary? Or are they strong enough as consumer brands to compete solo?